Banking is about to undergo a major shift. Whether we bank in person, over phone, online or mobile, our relationships with banks have not changed much alongside technological advancements. With the arrival of Open Banking, all that is going to change.

One of the key developments emerging during the last couple of years has been the concept of Open Application Programming Interface (API) for use in the banking industry. Open banking involves opening up the APIs to third parties (financial technology-based companies), who can use the shared consumer data to create innovative products and services as well as generate offers and discounts based on consumer spending habits.

The API will enable the company software to access information from the software at another company. When we order an Uber, the Google Map's API helps us track our car's progress towards the pickup point.

Without these APIs, if you want to share the data in your bank account with another company, you have to actually give them your login details. These new APIs will allow you to share the data in your bank account safely and securely, without having to hand over your password.

The goal of Open Banking regulations is to transfer ownership of account information from the banks to the customers. It lets people securely share their own transaction data with other banks and third parties.

The fundamental part of open banking is that, the customer is not bound to share his data with a third party if he does not want to. Each provider will ask for your consent to access your info when you sign up to it. It will then send a request to your bank, which will process it and then share your details. You can also withdraw your permission at any time. The rules only apply to accounts which can be accessed online, and you'll need to connect your online banking with the third party so that it can get your data.

Ultimately, whether or not you share your data is totally up to you. But it is worth knowing that under Open Banking, your financial data will be more secure than ever before. All banks, apps, companies and other third parties operating under the Open Banking structure are measured according to the highest standards of privacy and security.

Here are just a few real-life ways through which the customer could get benefit:

- Get better deals on credit cards, loans, and mortgages by easily comparing them across different financial institutions and third parties based on the customer's personal circumstances.

- Get a clear view of accounts in one place.

- Easily monitor various bank accounts and credit cards for any fraud.

- Use a single platform to easily and securely manage money across various services and providers, from banking to online shopping.

Open banking is not just for developed countries; many other markets around the world have been looking to adopt similar principles with the ultimate aim of delivering better financial outcomes for the customer.

HAPPENINGS AROUND THE GLOBE

Europe: Open Banking is a series of reforms on how banks deal with client's financial information. On January 13, 2018, after more than two years of planning, the Payment Services Directive2 (PSD2) arrived in Europe. This directive has for the first time forced European banks to open up their API's to fintech (financial technology) and other financial companies. As a result, PSD2 is changing and will continue to change the relationships between consumers and financial institutes. The original Payment Services Directive (PSD1) was adopted in 2007 to increase competition in the European payments market and to strengthen consumer rights by implementing the same set of rules across the entire EU.

Britain is leading the move in adopting Open Banking worldwide. The United Kingdom's Competition and Markets Authority adopted a staged approach to Open Banking to allow for a smoother and lower-risk implementation of single API standard earlier this year.

America: The USA hasn't had such regulatory pressure. Signs that banks are opening up their data to third-party FinTechs are beginning to emerge, a trend partially attributed to competitive market pressures. Similar signs are popping up in Canada too. Large banks are entering into data sharing arrangements with individual partner organizations. However, there is no doubt that open banking will arrive in the USA in the not too distant a future.

As for Latin America, Mexico stands out after passing the fintech law, which gives fintech companies greater regulatory certainty around issues such as crowd funding, payment methods and crypto currencies. It lays the ground for Mexico to introduce an open banking regime.

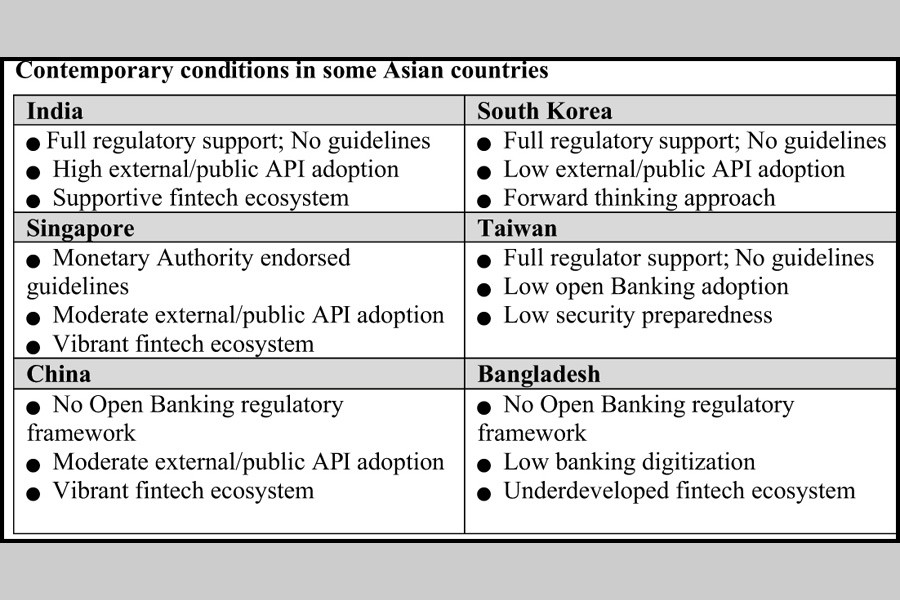

Asia: In 2016, South Korea was the first country to launch a common API infrastructure across their financial institutions. Singapore has recently been leading the way in open banking revolution. The Monetary Authority of Singapore (MAS) has been encouraging financial institutions to develop and share their APIs openly, so that they can work with other service providers to give customers a richer and more seamless experience. In other major economies like Japan and India, leading companies have taken steps to enable third-party data sharing in the absence of regulation.

Australia: Australia has moved one step closer to implementing an open banking regime with the publication of a final government report on the issue. Open banking in Australia aims to be a game changer leading to better deals on mortgages, personal loans and small business loans. Australia's four largest banks, viz. Commonwealth Bank of Australia (CBA), National Australia Bank (NAB), Westpac and The Australia and New Zealand Banking Group (ANZ), which hold around 95 per cent of market share, are set to enable open API access for customers this year. The national government budgeted AUS$1.2 million for the Treasury in 2017-8 to assess what the open API scheme should look like. The focus here is still very much on immediate payments but awareness on Open Banking and API has increased among Australian banks.

Africa: As one of the most mobile-first continents and given the significant unbanked population, open banking efforts have been heavily focused on providing alternative mobile solutions (e.g. M-Shwari, M-Pesa, Tala). Open Banking is the opportunity Africa needed to modernise the banking efforts and reaching the wider population. Open banking is particularly beneficial in unbanked areas of Africa, and telecom companies are acting as a vehicle for open APIs.

There are two preconditions for bringing Open Banking to Bangladesh: New regulations and the technology. Banks can focus on collaborations and adopt an ecosystem approach by adding third-party capabilities to their core business offerings and voluntarily opening up their APIs, thereby creating innovative business models and sources of revenue.

Our banks need to prepare for and embrace this paradigm shift, because it will foster innovation and provide greater value to customers. Every bank will choose different positions in the market based on their DNA.

In India, one of the early examples of open banking is Unified Payment Interface (UPI), an instant interbank payment system developed by National Payments Corporation of India. Whilst the regulators have not yet commented on open banking, a number of commentators have started noting that India is in an excellent position to carry forward open banking quickly. In the context of 29 states and 1.25 billion people, they have already implemented Aadhaar, a program to provide Indian citizens with a 12-digit ID code based on location and biometric data. Analysts say, an estimated 270 million bank accounts were opened using the Aadhaar payment app, meaning more transacting and banking is being done outside the traditional ecosystem. Now Aadhaar is the largest central database of biometrics-based identity information in the world.

There are a lot of supply challenges in the banking industry of Bangladesh. The cost of providing financial services is very high as against ticket of the product. Open Banking is the only solution to this problem.

Despite digitisation and open sources, sectors like retail, transport, food and beverage, education, etc. are all going through major disruptions. But the impact of the trend will be much larger on the financial services sector, and the business models based on them are on the verge of achieving digital transformation.

With Open Banking, there are multiple stakeholders involved in the business and there is little or no clarity on who owns the customer data or who should be accountable for data protection and security. It will be difficult to point out who owns all this data as it will continue to flow from one screen to another. Going forward, expediting data ownership and customer privacy is going to be very critical.

The changing banking landscape presents challenges, but also opportunities. Our banks should work with other service providers to give customers a richer and more seamless experience. Challenges and opportunities will emerge as the Open Banking community continues to grow throughout 2018. Data privacy, cyber security and customer protection must remain a key focus for banks throughout the implementation phase. However, the benefits that Open APIs can provide to customers and banks will drive their growth and adoption.

Md. Abdul Kader is Assistant Vice President & Head of Retail Credit, Southeast Bank Limited.