A recent World Bank (WB) report has revealed that nearly half of Bangladesh's population aged 15 or above remain without a bank or mobile financial service account. Lacking enough money has been the most commonly cited barrier to account ownership. It has also been said that men are more likely than women to have an account. While account ownership has surged in economies like Bangladesh, progress has been slower elsewhere, often held back by large disparities between men and women, the rich and the poor. The gap between men and women in developing economies remains unchanged at 9.0 per cent since 2011.

In Bangladesh, there remains a huge gender gap. While the percentage of men owning an account has risen from 35 per cent to 65 per cent in the last three years, the percentage of women owning an account has increased marginally from 26 per cent to 36 per cent. Similarly, while proportion of men owning an account at a financial institution has risen from 33 per cent in 2014 to 50 per cent in 2017, the proportion increased to merely 32 per cent from 25 per cent for women during this period. The relatively low uptake of account ownership is deemed to be a testimony to the persistent economic inequality in the country.

It is appalling that although financial inclusion is a key driver in tackling poverty and boosting economic growth, a staggering 1.7 billion adults remain unbanked across the world. Most of them live in low and middle income emerging markets, but large numbers of people are unable to use banks to meet their day to day financial needs even in high-income countries. Also, Bangladesh is among the economies where men are twice as likely as women to have access to both mobile phone and internet. But in developing economies, while 43 per cent of men have access to both these technologies, only 37 per cent have access in case of women.

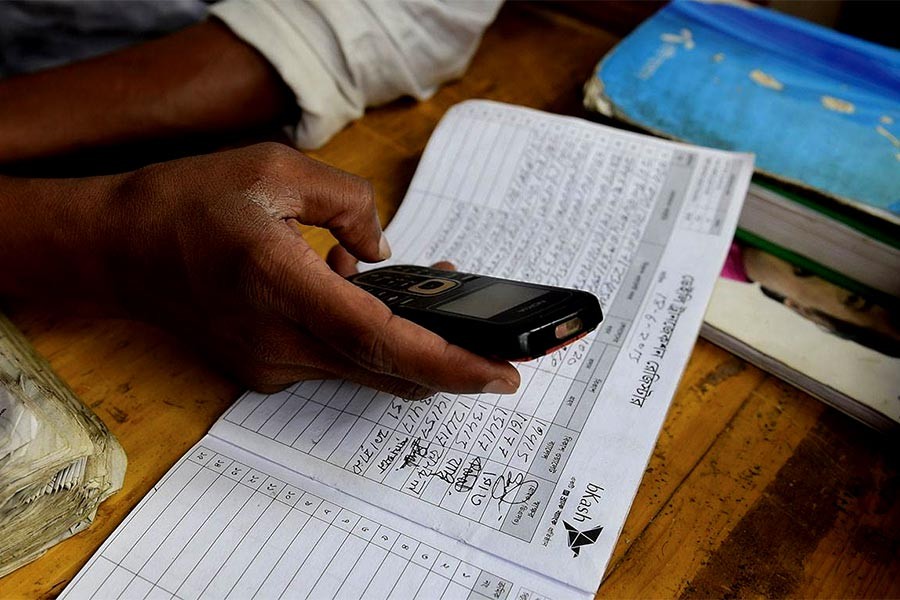

A smaller share of unbanked adults, not surprisingly, have both mobile phone and access to internet in some form-whether through a Smartphone, a home computer, an internet café, or any other means. Globally, this share is about 25 per cent. Large numbers of account owners, totalling 15 million in Bangladesh, receive cash payments for the sale of their agricultural products. The WB report says that digitising agricultural value chains offers multiple opportunities for increasing the use of accounts, not just through payments for the sale of agricultural products, but also through important related payments like purchase of crop insurance and agricultural inputs. Bangladesh is lagging behind tremendously as 69 per cent of adults across the globe - 3.8 billion people - now have bank or mobile money account, a crucial step in escaping from poverty.

Banks can adopt various schemes to help the unbanked households join the mainstream financial system. They can open special branch offices like outlets conveniently located for lower-income households, even when these branches do not meet standard profitability thresholds. These branches are often maintained to obtain a greater reach. Such initiatives may draw more of the unbanked into bank branches, offering them a tailored set of services. This can become profitable for the banks by gaining new account holders.

The economy can benefit greatly if women gain equal access to financial services. The impact was found to be amazing when the government deposited social welfare payments or other subsidies directly into women's digital bank accounts. Through this, women gain decision-making power at homes, and they invest in prosperity of their families with more financial tools at their disposal. This can also help drive broader economic growth.

Two-thirds of the 1.7 billion who remain unbanked globally own a mobile phone that can help them gain access to financial services. Understandably, digital technology can be leveraged to bring people into the financial system. It can also take advantage of existing cash transactions to further increase account use, as a large number of account owners in the country pay utility bills in cash.

It is high time that the government focused more on female entrepreneurship so as to encourage real economic empowerment of women. Also, digital technology can take advantage of existing cash transactions to bring more people under the financial system and thereby help achieve universal financial inclusion.