Currently, there are 64 banks in Bangladesh, including both scheduled and non-scheduled banks. With the recently approved Community Bank, 47 of them are scheduled commercial banks of which 41 are private commercial banks and six are state-owned banks. Since the year 2000, 17 new banks were given permission by the government. Previously, between 1990 and 2000, 18 new banks of different nature were allowed to operate in the country. It is imperative for the development of any country to strengthen the platform for trade and commerce through the expansion of financial institutions. It may, however, be mentioned that the rising GDP and growing population of the country may have prompted the emergence of banks over time under the successive governments.

The number of banks in the last 5 years has increased at a noticeable rate. 11 banks have been given permission since 2013 of which 10 are commercial banks and one is non-scheduled specialised bank. Recently, permission has been sought for another three new banks. If these banks get permission, total number of banks will be 67.

Normally, the number of banks in any economy depends on the supply and demand of different types of deposit mix, loan instruments and financial services. The more the opportunity arises for higher investment and financial service, the higher the need for new banks. It is also important to account for the efficiency of different banks for the long run when the need of affecting the financial institutions becomes important. Recent proposals for new banks have raised concern among economists and banking experts because of the burden these banks may create for the economy. They have questioned the relevance of these banks given the population size of Bangladesh and the current inefficiency of the existing banks, particularly the few fourth generation banks.

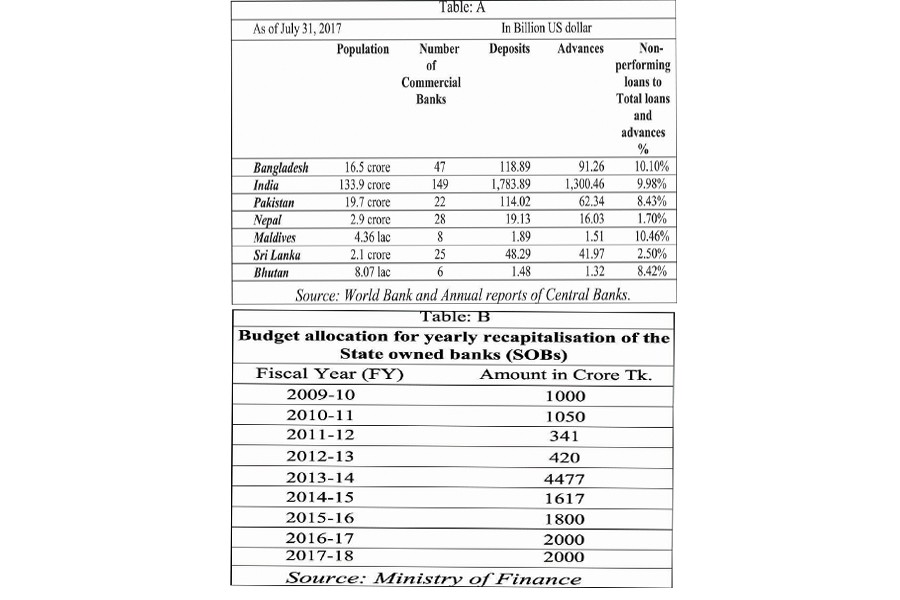

If the SAARC region is taken into consideration, we can have interesting insight as to what determines the number of banks in the SAARC countries -- the size of the population or other factors.

Among the SAARC countries it seems that the number of banks does not depend on the size of the country in terms of area rather on the amount of deposits or other factors. Even though Pakistan is a larger country than Bangladesh, the number of commercial banks is lower than that of Bangladesh. There are many micro-finance banks in Pakistan which are able to meet the need for extra commercial banks. As of 2018, the number of schedule commercial banks in India is 149 which is due to their large deposit and loans in the economy. Interestingly, Pakistan has a lower number of advance and deposits compared to Bangladesh up to fiscal year 2017.

Regarding the addition of new banks in Bangladesh, the question whether they will be able to run smoothly without being a burden has remained unanswered. State owned banks are already stuck in inefficiency and corruption for which huge capital has to be injected by the government every year in order to help them ride out their capital crunch.

Recapitalisation of state owned banks by the government has often been met with criticism. Table below presents a glimpse of recapitalisation:

With all these drawbacks in the banking sector, inclusion of more banks obviously won't go without criticism. Proper measures must be taken to identify whether the necessity is to satisfy the profit of banks or accommodate the rising demand of loans and deposits. Political consideration must not be a factor here at all.

The government should explore the situation pertaining to new banks in the light of the experiences of our neighbouring countries. At the same time, the government should encourage the existing banks to formulate innovative mechanism to explore the unbanked regions of the country. Existing banks can extend "agent banking" facility to the remote corners of the country. Already established banks can exploit their experience in developing "focused banking" to create the entrepreneurs through lenient loan facility and easily accessible information. Mobile financial services (MFS) similar to Bkash have a pivotal role to play, especially in rural areas. The commercial banks have now realised the potential of mobile banking products and services to enable the rural people for accessing financial services. The spreading of mobile banking products and systems will definitely contribute to erase the rural-urban divide and integrate rural economy with global economy.

Possible alternative to more commercial banks can be merging and acquisition of poorly performing banks. In this regard, Bangladesh Bank and the finance ministry should pay attention to the types of loans, deposits and borrowings these banks intend to capitalise on. The relationship between the number of banks and the performance of the banking sector should be properly investigated into before deciding on more banks.

Syed Md. Aminul Karim is former Member, NBR and Md. Ariful Islam is a banker.