Borrowing from the formal banking channel has been difficult for small enterprises for unclear definition, lack of required documents and deficient bank-client relationship, speakers told a programme on Saturday.

Even complicated disbursement process, absence of bank account, minimal scope of collateral have also been creating barriers for cottage, micro, small and medium enterprises (CMSMEs) to get loans, they said.

The observations came at a workshop styled 'Procedures and Preparedness for CMSMEs to Get Loans from Stimulus Package' hosted virtually by the Dhaka Chamber of Commerce and Industry (DCCI).

Bangladesh Bank general manager (SMESPD) Jaker Hossain addressed as the guest of honour while DCCI president Rizwan Rahman gave a welcome note at the event moderated by DCCI senior vice-president Arman Haque.

Islami Bank Bangladesh Ltd executive vice-president Md Rafiqul Islam presented a keynote during the programme.

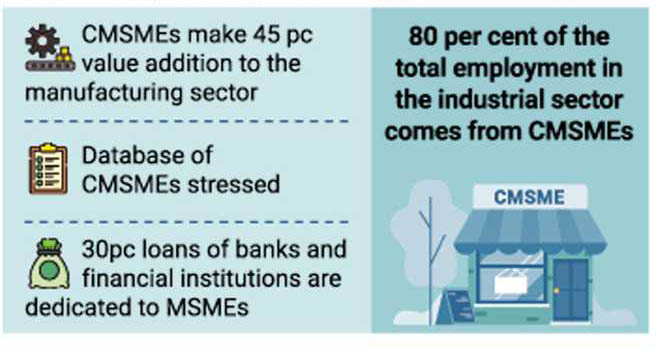

DCCI chief Mr Rahman says almost 80 per cent of the total employment in the industrial sector comes from CMSMEs making nearly 45-per cent value addition to the manufacturing sector.

But for want of fiscal and policy support, he asserts, CMSMEs can hardly utilise their full capacity and potential to grow further.

Citing the Tk 400-billion state stimulus for CMSMEs for pandemic recovery, Mr Rahman says intricate definition of CMSMEs, insufficient papers and complex disbursement process impose constraints on their getting loans.

Even many micro-enterprises do not have bank accounts while others' relationship with banks is not that sound enough to build trust for borrowing.

Unavailability of a CMSME database and issues related to collateral can also be underlined as limitations for the sector to get the government's financial support.

Referring to the state of the stimulus payout for CMSMEs, central banker Mr Hossain says loan disbursements are quite satisfactory in city areas, but rural businesses are somewhat lagging behind.

Nearly Tk 155 billion (77.5 per cent) has been disbursed from the first Tk 200-billion bailout and Tk 62.17 billion (31.08 per cent) from the second package, he discloses.

According to Mr Hossain, there might be some misconceptions among bankers and entrepreneurs at field level which are slowing down the disbursement process.

Mentioning that banks are rather aggressively looking for CMSMEs instead of reluctance to give loans, he calls for loan-seekers to submit proper documents and cooperate with banks for the purpose.

About the definition of CMSMEs, Mr Hossain says, "It will be redefined in the next industrial policy as we have to promote and facilitate real SMEs…"

He requested bankers not to harass any loan-seeker.

Meanwhile, the keynoter hammers home the importance of a CMSME database for lending as small enterprises represent almost 90 per cent of the total businesses.

Formal SMEs contribute up to 40 per cent of the GDP in emerging economies, he says.

A business needs to be categorised under a specific segment to get loans easily, Mr Rafiqul adds.

Terming Bangladesh Bank's policies very flexible, he says as per the regulatory guideline, 30-per cent loans of banks and financial institutions are dedicated to micro, small and medium enterprises.

Mentioning that bankers have to follow 86 rules and regulations, Mr Rafiqul says a minimum set of documents is needed for a CMSME loan to ensure transparency.

To this end, he suggests digitalising all services as banks are ready and willing to disburse loans, although the number of proposals is still not that much.