Eastern Bank Limited (EBL) has continued to strike a balance between liquidity, profitability and solvency to post a positive growth in the first half (H1) of 2021 calendar year.

The private commercial bank (PCB) has shown this performance when the overall financial sector is struggling with rising default loans, shortfall of provision and capital, shrinking profitability, operating inefficiency and weak governance.

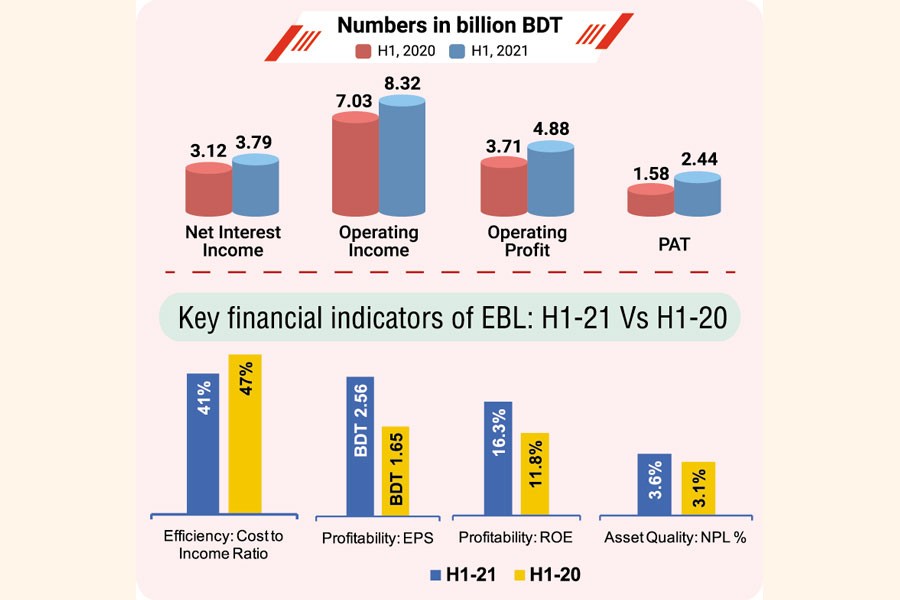

EBL’s strong focus on asset quality has driven it to achieve low non-performing loans (NPLs) of 3.60 per cent at the end of June 2021. The bank's NPL percentage is far below the industry average of more than 8.0 per cent, the bank’s data showed.

However, its net NPL ratio, which is measured by netting off specific provision and interest suspense from NPL, was 1.27 per cent at June end 2021.

EBL has also kept excess provision of Tk 1.79 billion (Tk 179 crore) in addition to classified loans requirement for strengthening shock absorbing capacity under stressed scenarios resulting in NPLs coverage ratio of 143 per cent during the period under review.

The PCB’s cost to income ratio, a measure of operating efficiency, improved significantly in the first six months of this year to 41 per cent from 47 per cent in the same period of 2020.

Cost to income ratio improved due mostly to higher operating income growth of 18 per cent, driven mainly by 21 per cent growth of net interest income, in H1 of 2021 than operating expense growth of 4.0 per cent over those of the same period of the previous calendar year.

EBL reported profit after tax per employee, a measure of productivity, at Tk 1.30 million (Tk 13 lac) in 2020, one of the highest among peers.

However, the net profit after tax (consolidated) of EBL stood at Tk 2.44 billion (Tk 244 crore) in the first six months of 2021, up by 55 per cent year-on-year.

EBL’s intrinsic and relative financial strength is largely a result of its solvency (indicated by its shock absorption capacity relative to its risk) and its liquidity, according to senior executives of the bank.

During the period under review, the leading PCB maintained capital-to-risk weighted-assets ratio (CRAR) at 13.91 per cent against the regulatory requirement at 12.50 per cent, Tier-I Capital to risk weighted assets (RWA) ratio of 9.98 per cent against such requirement at 8.50 per cent including capital conservation buffer and leverage ratio of 5.78 per cent against requirement at 3.0 per cent.

“Our focus has always been to conduct business prudently within the regulatory framework,” explained Ali Reza Iftekhar, managing director (MD) and chief executive officer (CEO) of EBL.

Meanwhile, EBL has been able to manage all the major regulatory liquidity ratios during the period. The second generation PCB maintained liquidity coverage ratio (LCR) at 143.10 per cent as against minimum requirement at 100 per cent in H1 of 2021.

Besides, the advance-deposit ratio (ADR) of EBL stood at nearly 80 per cent during the period against the regulatory maximum ceiling of 87 per cent, meaning EBL has still room to grow as far as ADR ratio is concerned.

The central bank of Bangladesh had earlier set the safe limit of ADR at 87 per cent for conventional banks and at 92 per cent for Shariah-based Islamic banks.

At the end of June this year, EBL maintained excess cash reserve ratio (CRR) of Tk 3.97 billion (Tk 397 crore) on bi-weekly basis and excess statutory liquidity ratio (SLR) of Tk 23.11 billion (Tk 2,311 crore) against regulatory requirement which indicates its strength in liquidity position.

Though EBL posted positive cash flow of Tk 1.87 billion (Tk 187 crore) from profit and loss (P&L) items in the first half of 2021, cash flow from operating activities was negative by Tk 8.83 billion (Tk 883 crore) since asset growth was funded mostly by borrowing.

As borrowing is a component of financing cash flow (not operating cash flow), operating cash flow tends to be negative if loan growth is funded by borrowing instead of deposit.

However, positive cash flow of Tk 1.87 billion (Tk 187 crore) from P&L items indicates that the sum of interest receipt, fees and commission receipt, capital gain and dividend receipt was higher than the amount of interest payment, overhead and other operating expense plus tax payment during the period under review.

About negative cash flow, Mr. Iftekhar said: “EBL in its history has never been in a liquidity crunch. Our strong retail presence as one of the leading banks, access to development funds provided by Bangladesh Bank and development financiers, partially offsets funding risks.”

In the first half of 2021, EBL followed a cautious business growth strategy with the focus on alternative investment where credit risk and provision requirement are low.

At the end of June 2021, the PCB’s total assets increased by Tk 19.51 billion (Tk 1,951 crore) or 6.0 per cent; among those investment in the government and non-government securities increased by Tk 10.84 billion (Tk 1,084 crore) or 16.0 per cent and loans and advances increased by Tk 11.22 billion (Tk 1,122 crore) or 5.0 per cent.

“This balanced growth has generated positive returns for the stakeholders,” a senior executive of the bank noted.

EBL continues to maximise wealth for its shareholders by improving return on asset (ROA) to 1.40 per cent in the first six months of this year from 0.92 per cent a year before while return on equity (ROE) rose to 16.29 per cent from 11.78 per cent.

However, earnings per share (EPS) of EBL rose to Tk 2.56 in H1 of 2021 from Tk 1.65 in the same period of 2020.

EBL has, meanwhile, declared 35 per cent dividend for the year 2020 to the shareholders, which is the highest in the industry.

The credit rating agency CRISL has reaffirmed the Long Term rating “AA+” and Short Term rating “ST-1” of EBL with “stable” outlook. The international credit rating agency Moody’s also assigned “B1” rating to EBL with “stable” outlook.