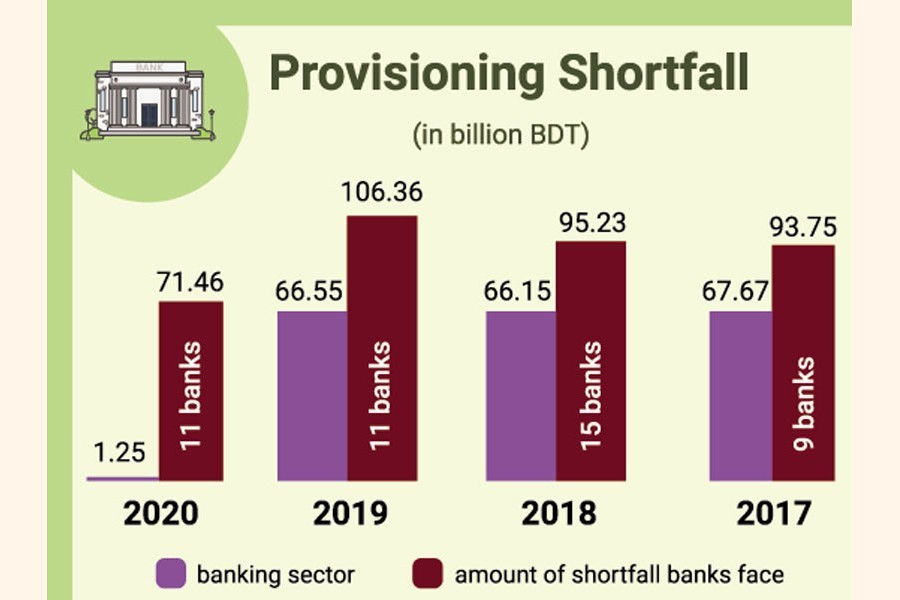

The provisioning shortfall against loans in the country's banking system fell by over 98 per cent in the last quarter of the year 2020 as the non-performing loans (NPLs) declined to some extent, officials said.

It came down to only Tk 1.25 billion in the Q4 from Tk 66.55 billion in the same period a year before, according to the central bank's latest statistics.

The calculation, however, excluded the offshore banking operations of the scheduled banks.

" The provisioning shortfall has declined in 2020 as the volume of NPL was much lower during the period under review," a senior official of the Bangladesh Bank (BB) told the FE on Wednesday.

Yet in such a comfortable situation, as many as 11 banks failed to maintain the required provisioning particularly against classified loans.

Out of the total 59 banks, three state-owned commercial banks (SoCBs), six private commercial banks (PCBs) and two development finance institutions (DFIs) could not provide for their respective NPLs in the Q4, according to the officials.

The combined shortfall of these banks stood at Tk 71.46 billion at the end of the year.

In 2019, most of these banks had failed to provision their NPLs fully.

The NPLs fell by more than 6.0 per cent or Tk 60.49 billion to Tk 882.82 billion, excluding offshore banking operations, as of December 31, 2020 from Tk 943.31 billion a year ago, the latest BB data showed.

The suspension of the usual practice of classifying loans that had been put into effect by the BB in March 2020 following the outbreak of Covid-19 was largely responsible for the shrinking of the default loans in the country's banking sector.

The banks have the scope of reducing their provisioning shortfall by reducing the classified loans or increasing the eligible collateral against credits, the central banker added. "The banks may reduce provisioning shortfalls with their net incomes too."

As per the regulations, the banks have to keep 0.25 per cent to 2.0 per cent provisions against general category of loans, 20 per cent against substandard category, 50 per cent against doubtful loans, and 100 per cent against bad or loss category of loans.

The banks usually keep the required provisions against both classified and unclassified loans from their operating profits to mitigate risks.

"The banks will have to enhance profits for reducing their provisioning shortfalls," said Syed Mahbubur Rahman, former chairman of the Association of Bankers, Bangladesh (ABB).