Non-performing loans (NPL) in Bangladesh's banking sector decreased by 1.20 percentage points to over Tk 1.20 trillion at the end of last December, following a special classification that economists see as transient cure.

According to Bangladesh Bank (BB) data released Sunday, the ratio of bad loans or NPL stood at 8.16 per cent out of the total loans and the classified loans came down by Tk 137.39 billion from the previous quarter (July-September) when the volume of NPL was Tk 1.34 trillion or 9.36 per cent of the total loans.

However, the overall figure of classified loans increased by Tk 170 billion on a year-on-year basis as the size of NPL in the banking sector was recorded at Tk 1.03 trillion as of December 2021, according to BB statistics.

The data show that the total loan disbursed was Tk 14.77 trillion at the end of December, of which 8.16 per cent became classified.

The highest volume of classified loans was recorded in state-owned commercial banks which saw repayment default on Tk 564.60 billion as 20.28 per cent of their total loans of Tk 2.78 trillion became defaulted.

The rates of NPL in specialised banks, private commercial banks and foreign commercial banks were 12.80 per cent (Tk 47.09 billion), 5.13 per cent (Tk 564.38 billion) and 4.91 per cent (Tk 30.48 billion) respectively.

On the other hand, the overall loan-provisioning shortfall in the banking industry narrowed to Tk 110.09 billion as of last December. It was Tk 135.30 billion at the end of September 2022.

The volume of overall loan-provisioning shortfall of state-owned commercial banks stood at Tk 88.28 billion and in private commercial banks at Tk 27.45 billion as of December last.

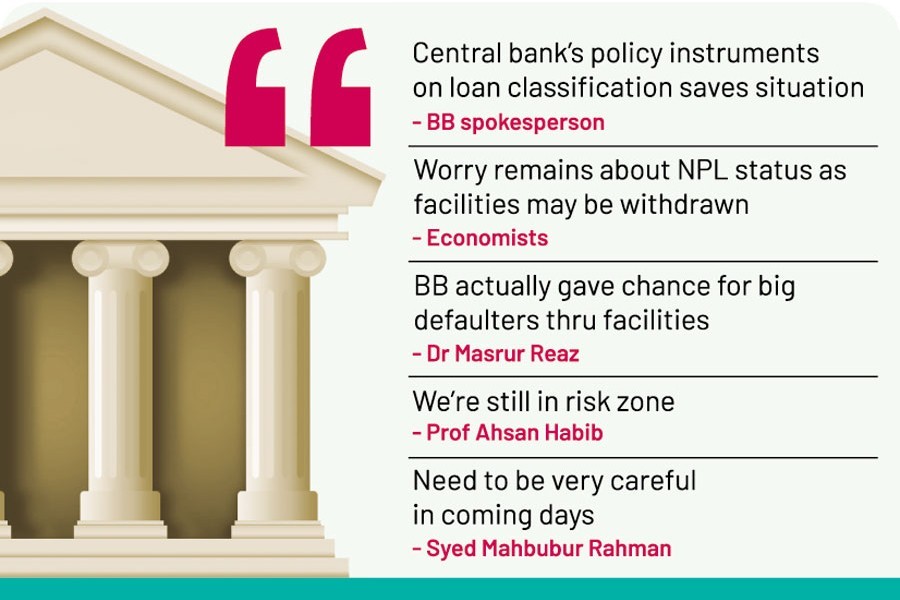

When contacted, BB spokesperson Md. Mezbaul Hoque said the economy is under pressure because of the volatile global geopolitical situation in the wake of Covid-19 pandemic and the ongoing war in Europe. Under such circumstances, the central bank took various policy instruments in terms of loan classification that helped improve the situation.

For instance, he said, the banking regulation and policy department earlier had issued a circular directing that if half the loan installments (50 per cent) are paid by December 2022, the loans would not be marked as classified. Earlier, minimum 75 per cent of a loan installment had to be paid to avoid getting in the trap of classification.

However, economists, bankers and academics familiar with the developments in the banking industry told the FE that the NPL situation improved on a quarterly basis due to some favorable measures undertaken by the central bank.

Yet they are worried about the NPL status as the facilities given by the Bangladesh Bank may be withdrawn.

Talking to the FE over the latest situation of classified loans, managing director (MD) and chief executive officer (CEO) of Mutual Trust Bank (MTB) Limited Syed Mahbubur Rahman said it is appreciable that the volume of classified loans has declined in comparison with the July-September period but the concerning fact is that it is still on the rise on a year-on-year basis.

"Decline is a good thing but we need to know what particular factor helps reduce the volume. Is it cash recovery, normal rescheduling or the non-classification facility for paying half of the loan installments? If we know that, we will be able to take measures accordingly," he said.

"But we need to be very careful in coming days," he added.

Dr M. Masrur Reaz, chairman of the Policy Exchange of Bangladesh, was critical of the facilities handed out by the central bank for tidying the bank's financials.

"To my mind, the facilities have actually helped improve the situation," he said.

The economist said the BB actually had given the chance for the big defaulters through the facilities. "Actually banks have been losing assets through such facilities."

He notes that such facilitation, on the other hand, erodes profitability and breeds risk for future funding for the economy.

Dr Shah Md. Ahsan Habib, a professor, and director at the Bangladesh Institute of Bank Management (BIBM), thinks there is still no sigh of relief on the fall in the NPL rate. "We are still in a risk zone unless we can improve it significantly."

He mentioned that all banks around the globe are not in the comfort zone now because of the Ukraine war-and the covid-19-related problems, and the banking industry in Bangladesh also remained in the uncomfortable zone.

"We need to take the right directions and take more measures to combat the NPL problem," the banking academic says. He notes that a shortfall in provisioning is not a good sign for the banking industry as well.

[email protected] and [email protected]